Climate change – and the actions required to solve it – is a widely acknowledged challenge. However, the relationship between those who cause the problem and those who bear the risk is not symmetrical, calling for collective action involving all parts of government, commerce and civil society.

Although sector pathways are starting to emerge, corporate action ranges significantly across and within sectors, and between countries. For example, some large technology companies have net zero targets including negative emissions and compensation for historic emissions, while others have 2050 net zero targets, and others have no targets at all. These differences generate a significant range of carbon buying strategies, from none to market leading. The first mover here is a leader, but, unless, all the players participate, leadership fails to produce the intended environmental benefits and a scaled market.

Additionally, markets or governments do not price carbon effectively as an externality, which caused carbon pricing to be immature and to vary significantly. Hence there is no immediate and monetised incentive to take part in carbon markets. This is not unique to carbon markets but is felt most acutely because carbon units are treated as an expense, with little utility outside of voluntary claims (albeit this is not clear, see Section 5.2) and a general contribution to meeting planetary climate goals.

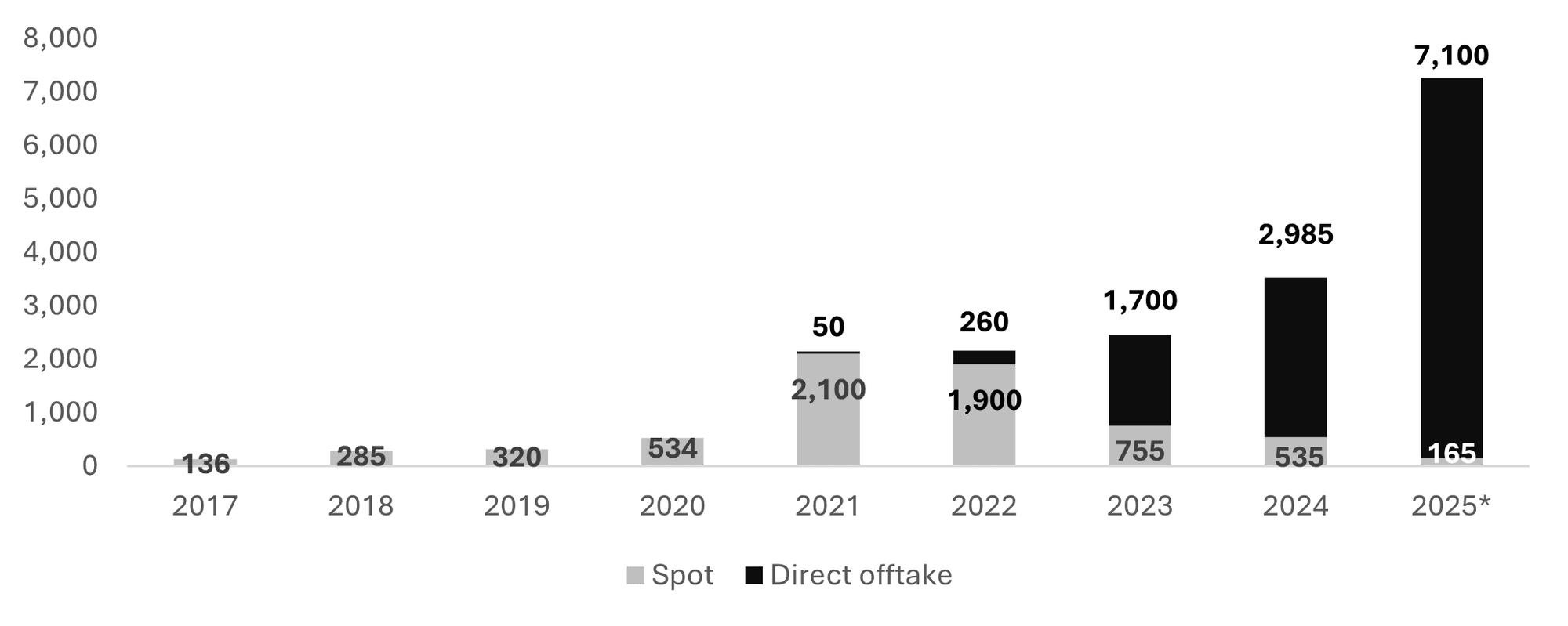

ETS carbon prices vary widely from US$1tCO2e through to US$167tCO2e,24 with very significant dilution of many carbon prices per tonne, due to sector coverage and free allowances. Furthermore, because carbon taxes have historically largely been separated from carbon credits, emitters pay to pollute, rather than invest in projects (as outlined in Section 1). This is, however, changing globally: 66 countries currently have a carbon tax or ETS in place.25